Prepayment from Home loans Norms, Charge & Most other Facts!

Gamble Miss Cat Slot

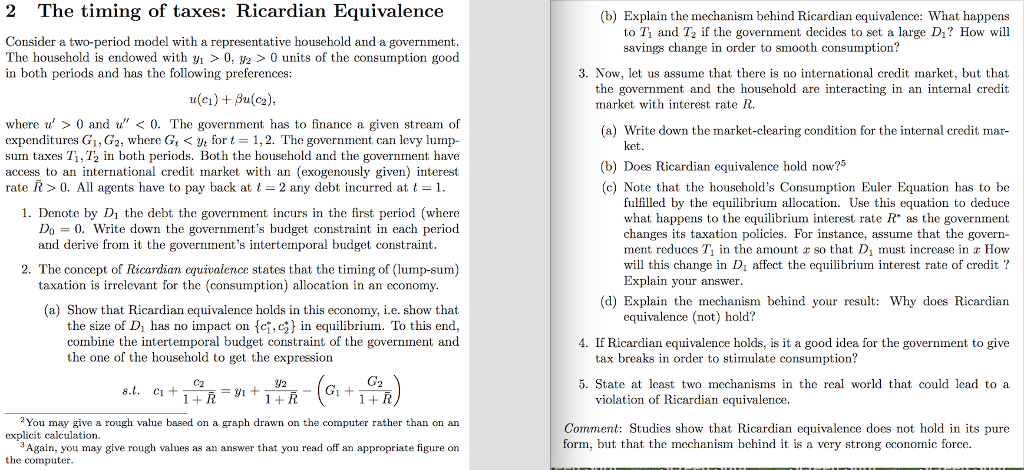

14. Januar 2025Nfl Opportunity, Playing Lines and you can Point Advances

14. Januar 2025Home financing, that’s usually pulled for as long as 20-3 decades, may have huge desire loans to own a borrower meet up with. But the duty are shorter to some degree if you utilize the prepayment studio one to banking companies and you may houses boat finance companies (HFCs) promote to help you borrowers.

Loan providers supply the prepayment facility toward borrowers with which it can make region otherwise complete fee of their amount borrowed prior to brand new repaired tenure chosen by the all of them. This helps borrowers in lowering both the focus and you will dominating the matter across the tenure.

In this post, we will be letting you know everything pertaining to the latest Prepayment off Financial – what is a prepayment facility, the amount of money it can save you from this, and concerning prepayment organization of your own ideal mortgage lenders. Continue reading to know a lot more!

While we told you just how home loans usually are drawn to possess a longer time period whenever just one opts for a mortgage, the newest payment is completed thru Equated Monthly installments (EMI). Which EMI number consists of part of the primary amount and you may attract amount. Such-like choosing a longer period, the interest count is highest correctly.

And when just one ount along side financing tenure and reduce the overall mortgage load, this new business you to definitely an individual opts is known as Prepayment Business. Using this, an individual may shell out an additional quantity of prominent over and you can a lot more than your own typical EMI number in the some other issues on your own tenure. If this is completed when you look at the short parts, it is known as an ingredient-prepayment Studio. Very, whenever just one pays some additional amount anytime http://cashadvanceamerica.net/payday-loans-ar in the way of one’s financing, the main outstanding number commonly instantly decrease, by virtue of these, your own EMI otherwise mortgage tenure normally smaller.

Prepayment of Lenders Norms, Costs & Other Information!

If you are going for the newest prepayment from mortgage, it is important to check out the fees on prepayment facility. Lenders usually do not charge on prepayment in case the home loan is pulled towards a drifting interest, however, if the mortgage is taken on a predetermined rate out-of interest and borrower would like to prepay the borrowed funds via refinancing (taking an alternative mortgage) then the costs usually consist of dos% to three% of your number getting prepaid service. Although not, there are no charge when your borrower is utilizing their otherwise her very own funds so you can prepay.

You will find yet another thing that you should know that it is best to make an excellent prepayment of your house financing on 1st many years of the period. As to the reasons? As the desire number could be into the increased front within these age and slowly get smaller as the ages citation from the. Thus, to keep with the attract matter, it might be better if one prepays our home financing about initially years.

Impression off Prepayment out-of Home loan in your EMI amount and you may Mortgage Tenure

Mit dem Laden des Videos akzeptieren Sie die Datenschutzerklärung von YouTube.

Mehr erfahren

It might be best to understand the feeling of one’s prepayment studio thru a good example because to assist you choose greatest whether to do it or not. We are offering the exact same below. Have a look.

Suppose one has home financing away from INR forty-five lakh within a floating interest rate of 7.75% yearly to have a tenure of 18 many years. Therefore, considering these details, the brand new EMI number is INR 38,696. Some of the most other very important info are offered throughout the below dining table. Have a glance at them!

Today, after paying all of the EMIs punctually going back sixty days (five years), the new candidate desires build a part prepayment out of INR 5 lakh to minimize their dominating the matter.